By Deepak Kamlani, Inventures, Inc.

Introduction

In the nineteenth century, Karl von Clausewitz, the Prussian general, noted, “War is merely the continuation of policy by other means. Clausewitz made the observation for which he is known in a tumultuous era- the land grab times of Napoleon, the resulting military alliances between Prussia, Russia, and Great Britain, and, of course, Waterloo, a battle in which he fought. These events have loomed large in the evolution of Europe through the nineteenth century, and they undoubtedly helped shape the political, economic, and military landscape on the continent in the years leading to the Great War. It can be postulated that their implications are still being felt.

Clausewitz’s observation appears to have particular resonance in the technology world. While traditional blood and bombs wars between nations still occur, some of the nastiest and most brutal battles are bloodless- they take place between commercial entities, and they are centered on technology. In this landscape, companies resemble countries, technology is the policy piece, standards are the lingua franca of a huge and lasting land grab opportunity (essentially, the equivalent of the Versailles or Malta Pacts here), and business models approximate Waterloo- they succeed or fail based on the technology choices and alliances a corporation makes. So, we can paraphrase Clausewitz this way: “Standards are merely the continuation of Darwinian competition by hidden means.

The implications for a modern-day CTO or CIO are significant. In this article, I attempt to highlight the drivers for the creation of standards; their essential role in competitive technology strategy, particularly the generation of disruptive business models; and the key standards issues a CTO or CIO should consider as they develop technology strategies correlated to their supplier, partner, competitor, and employee value chains.

Standards and Market Development

It is difficult to argue against standards; perhaps it is just as difficult as arguing against national public holidays. After all, on the demand side, corporate and consumer buyers consistently point to the need for standards-based solutions, to ensure that they are not tied to any one supplier's proprietary technology and the resulting potential for predatory pricing tactics. Nor do they want to be limited to working in de facto technology islands, where they can only implement products manufactured by one supplier to ensure employees, partners, and suppliers can communicate to get business done. Their goal is to protect and leverage corporate capital investment in new technologies and select best-of-breed solutions that support core corporate objectives- and this requires products manufactured by many different suppliers to interoperate, or interwork, with each other.

A good standard delivers the substrate required to meet these objectives. At the highest level of abstraction, standards specify the hardware and software actions that, if implemented as specified, provide for a ‘plug and play’ buyer experience. A good purchase experience is proven to spur market development and brand loyalty- and therefore trigger market share, revenue, scale, and margin levers among all suppliers. Ethernet, TCP/IP, and Group III fax are traditionally cited as good examples of this effect. We can, I believe, include User Interfaces like the telephone keypad and QWERTY keyboard in this mix- they work everywhere in the world without any special training or knowledge other than the ability to push clearly labeled buttons. So, a standard and accompanying business model that drives these conditions can have tremendous monetary value and can, in turn, drive market capitalization. Shareholders like this value chain- increasing the value of equity is the one quantifiable measure by which a Board and its management team can be measured in objective terms.

Standards, then, make sense also on the supply side- they can and do provide a clear path to ubiquity, volume deployment, and RoI. Unfortunately, there are three parallel ways to enable these conditions. Standards come into being through ‘brute force/right place/right time/right solution’ factors and achieve de facto status per Windows, Linux and Mac operating systems; they can achieve consensus status through formal ratification processes defined by entities like the ITU, IETF, ISO, and National Bodies per Internet centric communications protocols like H.323, SIP, MPEG; or, they can achieve du jour status through the creation of a collaborative community of companies dedicated to developing missing standards and specifications or improving those that exist as a means to an end- namely market pull for Now products and services.

Our advice to a CTO or CIO would be to focus on the du jour community standards model as it offers the best risk-reward ratios, particularly in relation to time-to-return factors. De facto standards opportunities tend to surface at the rate of one per generation and, as such, are unpredictable in the ‘what-when-who-where-how’ stakes. Consensus standards opportunities are time-consuming, typically guided by politics at the national level (for instance, ITU standards votes are submitted by the Department of State in the US and its equivalent elsewhere), and they can be subject to non- negotiable Intellectual Property policies (e.g., royalty-free or open source) mandated by the standards body.

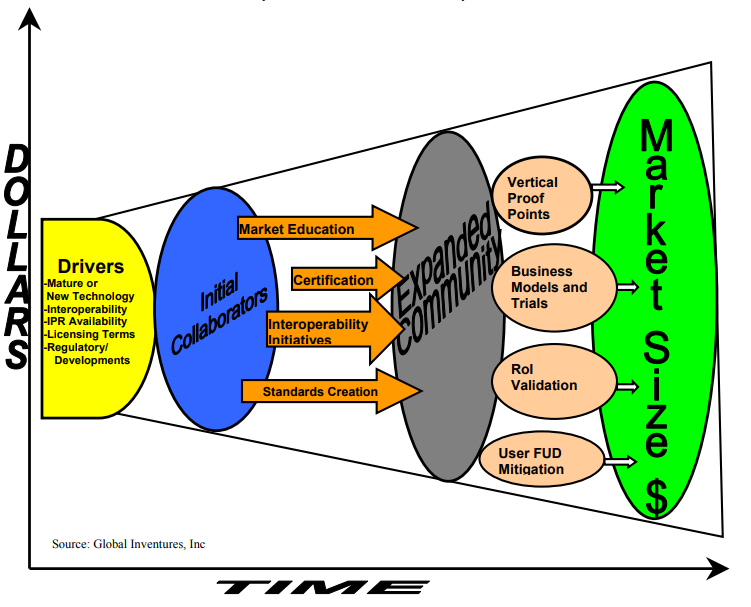

By contrast, as illustrated in Figure 1, du jour standards are built from the bottom up by one or more entities responding to or initiating specific business model drivers. These drivers typically address a new product/market opportunity that requires technology validation by multiple (ideally competitive) high profile market movers to stand a chance of success; a potentially high value category served by a mature technology and/or the availability of replacement solutions to challenge the status quo; implementation and interoperability concerns with current solutions; the availability of new Intellectual Property to disrupt existing (objectionable) licensing arrangements; or, opportunities arising from regulatory developments.

Figure 1

STANDARDS-BASED MARKET DEVELOPMENT

(COMMUNITY MODEL)

It should be noted that this community approach provides some guarantee of traction from the outset, because both early and future participants are aligned with the need for a new or replacement standard as a requirement for market development. So, the initiative is not about altruism or ‘doing the right thing’ per se. It is all about enabling the largest possible market as quickly as possible- and most importantly, about hedging risk. Our experience suggests that a given standard requires a minimum of $3 million in funding over a multi-year period to create the standard, launch interoperability and certification programs, educate and reach users, and mitigate the Fear, Uncertainty, and Doubt users typically have with trialing and deploying new technology. Few companies are willing to place that size of bet by themselves. A community of 50-100 companies, where each contributes an equal or higher share of the total funding required, allows for financial investment to be managed down to the $30-50K level per company, and the upside in guaranteed traction and total available market provides for a strong risk/reward ratio.

These factors, in part, explain the success that many community-driven standards initiatives have enjoyed in recent years. We repeat that monitoring or being actively involved in such initiatives should routinely be registered in a CTO or CIO's ‘must-do’ list of priorities.

Standards and Disruption

In a Utopian world, the model I have just described would perpetuate and replicate infinitely- markets would evolve through collaboration and coopetition between competing firms, there would be a singular a standardized development framework for each market segment, users and buyers would have assurance that products based on these frameworks would work together, and competition would be conducted on ergonomic, functionality, and price considerations. This is, of course, the win-win-win scenario everyone in technology worships.

Today’s real world, however, forces a CTO and CIO to choose between multiple technology options in every component of their supplier, partner, and employee business chain. So, communications backbones can mean IP, ATM, or PSTN. Computer Operating Systems can mean Windows, Mac, or Linux. Internet applications can mean Java or .Net. Voice and Multimedia applications on the Internet can involve a multitude of protocols- SIP, MGCP, H.323, and Megaco. Devices in a network can be discovered using OSGi, HAVi, or UPnP. Broadband can mean xDSL, Cable, or Satellite. High-speed networks in the home can mean HomePNA, HomePlug, Coax cable, and Ethernet. Wireless can mean Wi-Fi, Bluetooth, and WiMedia. All these acronyms are a de facto, du jour, or consensus standard- and they represent just the tip of the iceberg.

The pertinent question then is how and why these multiple standards emerged to address the same space. The answer is steeped in some irony. As I have noted here, standards activity is initially motivated by a pure thought- the need to unify and prevent market fragmentation along proprietary lines. Technology standards embody intellectual capital, so a win for one group of companies translates to a loss for others. A loss in this sense means a freeze-out, essentially an inability to address a market in a leadership mode and an inability to monetize available intellectual property- a.k.a. a blown business model. It follows that it is in the best interests of those left at the starting line initially to aggressively disrupt the adoption cycle of a new standard spawns. And the best disruption opportunity is --- another standard.

So, we are left with these conclusions:

- A successful standard will immediately provoke an equal but opposite response

- This is by definition an infinite loop, as the number of responses is limited only by the number of competing alliances possible

- The end result is fragmentation along competing standards lines versus proprietary technology

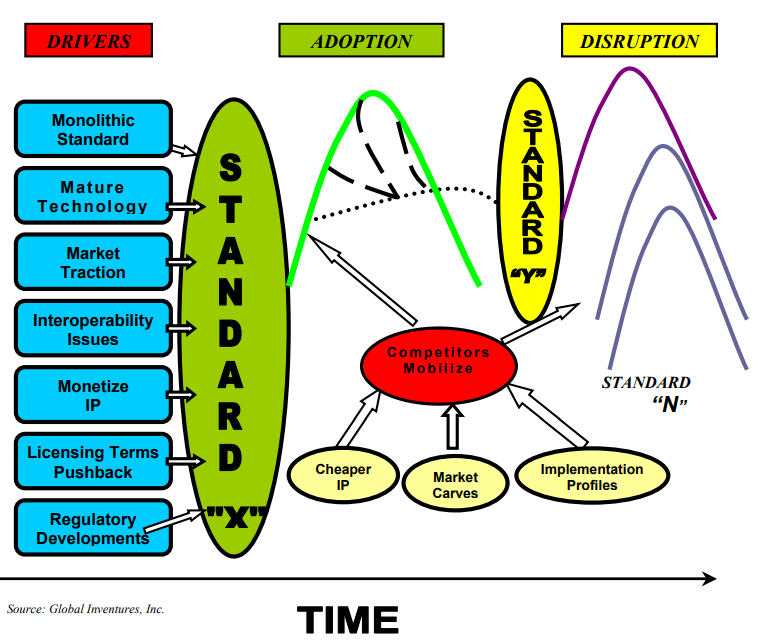

Figure 2 illustrates the Disruption Cycle from my perspective. Not surprisingly, the drivers for disruption are identical to the drivers for standardization activity. On the technology level, collaborators tend to characterize an approved standard as monolithic and unable to scale down to emerging applications, as mature, as having failed to gain sufficient market traction (or too much), or as having failed to solve interoperability issues. On the commercial level, the drivers relate to the need to monetize their intellectual property, mount a challenge to IP licensing terms put in place by the current IP holders, or an opportunity to leverage regulatory developments for competitive gain.

Figure 1

DISRUPTION EVENT CHAIN

Whatever the driver, competitors to an approved standard mobilize early in the market cycle and commercial adoption curve. Their efforts can be:

- Unsuccessful. Supporters of Standard X respond by exploiting their market lead to gain design wins and commercial mandates, thereby marginalizing the replacement effort.

- Somewhat Successful. Supporters of Standard Y are able to flatten or slow the Standard X adoption curve by embedding their IP in a new version of the standard- version X.Y- or profiling Standard X to include some of the Standard Y IP for specific commercial applications- Standard X.Y(vertical).

- Totally Successful. Standard Y acts as a substitute for Standard X, with new IP, Licensing Terms, and development substrates. These last only as long as Standards Z through N come into being.

In our experience, outcome 2 occurs most frequently- but not always. Because opposition to an approved standard typically begins after some commercial traction and design wins, but after significant product development cycles, the existing standard has a support base that can be leveraged. The developer and user communities recognize that a compromise is their only sure way of protecting their X investment and lobby for a complementary solution that allows X and Y to coexist. The inclusion of Standard Y concepts or accommodation of Y issues provides for a ‘peace with honor’ conclusion of hostilities and prevents a time-consuming and expensive outright war.

We can see this as the Beatles Effect (my preference) or the Brittney Effect (the choice my children would make). These are everyday world examples of disruption strategies – just as the Beatles spawned the Rolling Stones and each group in turn launched many ‘me too’ revenue streams for competing music labels, so a technology standard tends to follow a scenario where the Beatles and Rolling Stones equivalents can coexist.

How does this affect the CTO/CIO? I believe the following implications are relevant:

- Standards will continue to be created or morph and mutate to meet green-field and disruptive models, respectively. The challenge for the CIO is and will be to stay abreast of developments so the right technology choices can be made to meet internal user and external customer information and communication needs.

- Standards require customer validation to succeed, and that provides leadership opportunities for the CIO. Because traction and adoption are the proof points for a standard, a CIO can, in effect, function as a market maker for a particular technology. This also involves working at the bleeding edge, so the decision rests on the relative importance of leadership versus being a fast follower.

- A CTO must embrace and actively seek disruption as a baseline competitive technology strategy. I believe that this is particularly important for the CTO of a vendor company, in the ICT space. In our experience, service providers like the ILECs, ISPs, MSOs, and Utilities are usually content to consume baked standards as long as they have demonstrable development and supply-side support. As a vendor, absence from the baking party can lead to undefended and exposed technology positions and can therefore prematurely abort otherwise promising business models.

What remains is to examine the risk/reward matrix and investment required to incubate new solutions and/or disrupt those that exist.

Standards and Darwinian Behavior

Earlier, I referred to the dollars required to promulgate a standard and noted that spreading these dollars between 50-100 companies was one major advantage of a community-driven standards model. It is important to note that the minimum investment we believe necessary- $3 million- relates to the dollars that must be made available at the community level to establish neutral selection procedures, create and manage interoperability and certification programs, and perform marketing and buyer education. The fees that the community charges as a structured non-profit organization are allocated for these activities.

The investment required at the individual company level- particularly one with IP that is proposed for a standard- is considerably higher. A company in this position must consider both the hard and soft costs of driving the inclusion of its IP in the standard and the risk that the effort will not be successful.

We estimate that hard and soft costs, incremental to actual hardware and software development, range from $300,000 to $500,000 plus per year per company. This includes community membership fees, which range from $20,000 to $100,000 plus annually for a decision-making engagement; the cost of 2-3 volunteered Full Time Equivalent (FTE) resources to participate in Board meetings, Technical Committees where the scope and boundaries of the proposed standard are defined, make technical submissions, and active marketing and business development efforts; and travel and entertainment.

This represents Opportunity Cost, and for a small company, it is a significant drag on working capital. The drag magnifies in importance when the risk of failure in a Darwinian struggle is factored in. Although, as noted earlier, community-driven standards initiatives are the best chance of meeting market needs in a timely manner, this does not relegate the initiative to a rubber-stamp role. To the contrary, as illustrated in Figure 3, such initiatives develop beyond reproach vendor-neutral technology selection procedures and follow them to the law. This is necessary to ensure the community at large supports the selection and to positively affirm adherence to anti-trust guidelines. What transpires then is a 15-18 month process where:

- Competitors collaborate to specify Market Requirements for both current and future versions of the standards. This can include, at a minimum, disclosure of IP Licensing terms applicable in the event one submission is selected.

- An ‘open competition’ stage is invoked. Multiple submissions are invited and, when received, are subject to strict evaluation by an expert panel, validation through the delivery of prototype implementations, and field tests. In this stage, submitting companies face a Hobson’s choice- they must reveal their IP and technology in intimate detail to be considered, and they must be open to modification and change suggestions from competitors to avoid rubber-stamp concerns, but they must also accept that their effort may simply boil down to educating competitors if their solution is not chosen, and the modifications from others are incorporated in the final specification.

With the large investment and risk factors in play, can RoI be quantified? The qualitative returns are more easily identified than the quantitative returns. IP embedded in a standard carrier:

- ‘Bragging rights’ value for the winner, an important issue for an I/C company where technology is the name of the game;

- Time-to-market advantages relative to the competition, given that the underlying technology is homegrown and requires far fewer learn cycles for developers

- Differentiation advantages for the winners’ in-house and third- party partner implementations of the IP, as the case can be made that the implementations are derived from a gold cut of the IP.

The quantitative returns are more difficult to assess if the standard in question is not at the Windows or Java level in scope. We offer the following data points:

Video Compression. Created by the Motion Picture Experts Group (MPEG) for compression, transmission, and then decompression of digital motion video and audio signals for traditional video delivery, there are three MPEG video standards in use: MPEG-1, MPEG-2, and MPEG-4. In- Stat/MDR, a market research firm, estimates that the MPEG video chip market was worth more than $1 billion in revenue in 2001, with Unit shipments exceeding 100 million, and that in 2006, total shipments of MPEG video chips will reach 272 million units and $3 billion in revenue.

Video Conferencing. Defined as MCUs (Multipoint Control Units), which allow multiple parties to link together in video communications sessions, End-Points, which include videophones and video terminals, and conferencing service providers, the videoconferencing market is now a multi-billion dollar business globally. The emergence of key standards ratified by the ITU in the early and 1990’s- H.320, H.323, H.324- drove much of this growth.

Softswitches. ‘Softswitch’ is an umbrella descriptor for a software-based communications network that separates switching, or call control and services, from the underlying transport network. As such it is a radical departure from the traditional circuit-switched approach of combining transport hardware, call control, and service logic together into a single, proprietary piece of equipment. Standards created by formal standards bodies and community initiatives- H.323, SIP, MGCP, Megaco- provide a foundation for this evolving market, and In-Stat/MDR forecasts that the worldwide softswitch market is expected to reach $1.32 billion in 2006 and continue to experience strong growth beyond 2006 as the PSTN transforms to a packet infrastructure

Bluetooth. Bluetooth is a standard developed by the Bluetooth Special Interest Group for short- range networking. Allied Business Intelligence (ABI) projects Bluetooth chipset shipments to increase to 33.8 million in 2002, up from 11.2 million in 2001, and to grow to just over 1.1 billion chipsets by 2007, with associated revenues of $2.54 billion.

HomePNA. Developed through the du jour community model during 1998 and 1999, HomePNA 2.0, which allows for high-speed networking in homes over the PhoneLine without any new wires, has shipped in an estimated 5 million nodes. At an Average Selling Price of $70 per node, the total revenue generated from the standard is an estimated $350 million to date. The underlying Intellectual Property, which resides in chips, is worth perhaps 3-5% of the total.

These estimates and forecasts indicate the value standards can bring to markets and the revenue opportunity available to companies with early traction in the respective categories.

Summary & Conclusion

As I hope this article has shown, standards have high intrinsic value in setting corporate technology strategy and as a basis for disruption and competition. The markets spawned by standards can, as outlined above, generate the potential for large revenue streams, and the realization of market share and profits will typically accrue first to companies with the early mover advantages that community-driven standards initiatives provide.

The CTO, in particular, must consider the upfront investment required to harvest this opportunity in a du jour community initiative. As noted, this investment can total $1-2 million over three years, exclusive of engineering and development, and all the typical factors leading to a BOM (Bill of Materials). We offer the following decision tree:

- Consider whether you want to lead or fast follow. If the business model makes it essential to bake the company’s IP into a standard, and marketing, messaging, and competitive positioning also rest on this, the $1-2 million, multi-year commitment is necessary.

- Consider the disruptive value of decision-making power. While leadership may be preferred, the company may be behind the market and competition technologically. In this case, a decision–making role-which carries veto, slow down, and final approval rights, may be the appropriate engagement. The cost here is $50-100K per year, inclusive of all components.

- Consider the importance of time-to-market. If the sole interest is to adopt approved standards, the only commitment required is to participate and pay membership dues to an appropriate organization. At even the lowest level, membership usually provides early access to finalized standards and those in draft form. The investment here is perhaps $10K per year, for time-to-market advantages in product introduction and delivery relative to competitors not involved in a similar way.

When approached holistically, we believe that standards must register high in the priority chain for the CTO and CIO, and we repeat that they offer both the substrate to meet internal ICT needs and the drivers for competitive technology and business strategy.